|

The Week Ahead: Highlights

Asia-Pacific Preview

Watching for Another RBA Rate Hike

By Brian Jackson, Econoday Economist

The Reserve Bank of Australia policy meeting will be the

main focus. Officials have raised policy rates at each of their two previous

meetings and indicated that further policy tightening will be considered if the

inflation outlook does not improve. Since then, the spike in fuel prices caused

by the Iran conflict has pushed monthly inflation sharply higher, suggesting

another rate hike is likely next week. Australia will also report household

spending and trade data in the week ahead.

PMI surveys for April will also be a major focus in the

Asia-Pacific region. PMI surveys for China published this week showed mixed

results, but next week's reports should provide further information about the

impact of the Iran conflict on activity, sentiment and cost pressures in the

region.

Taiwan will report trade and inflation data next week, while

Hong Kong will publish its GDP report and New Zealand will publish quarterly

labour market data.

Europe Preview

After an Eventful Week, Eyes Turn to German Data

By Marco Babic, Econoday Economist

As the conflict in the Middle East enters its third month

with no signs of abating, last week's inflation data showed to what extent it's

impacting prices. Consumer inflation picked up to levels that are bound to make

the European Central Bank uncomfortable. While the ECB kept rates steady, as

did the US Federal Reserve, policy makers are facing a dilemma of combating

inflation and keeping tepid economic growth from turning negative.

Certainly core inflation rates which strip out the effects

of higher energy costs reflect more moderate inflation. In fact, falling energy

prices prior to the conflict have kept inflation muted. Still, higher energy

prices force consumers into choices on discretionary spending which will crimp

GDP. It's small comfort to consumers to hear that inflation excluding energy

and fuel is moderate. After all, inflation excluding everything is flat.

Germany will provide some clues as to how industry is coping

with the conflict. On Thursday, March factory orders are scheduled for release,

followed by industrial production on Friday. There has been some evidence that

production has picked up in other economies as businesses attempt to boost

inventory and, by extension, production to get ahead of expected price

increases for raw materials, particularly intermediate goods. At the same time,

they are ramping up production to keep up with orders. While increased

industrial activity is welcome, it would be increasing for reasons that are not

optimal.

In addition, trade data for France and Germany are released

Thursday and Friday, respectively for March. This could give indications of how

much has been affected by the conflict. The effect of tariffs which was such a

big talking point for months, now seems to have turned to a whisper.

Ultimately, the European Central Bank will likely be forced

to raise interest rates just at a time when economic growth is sluggish.

US Preview

US Employment Report in Focus

By Theresa Sheehan, Econoday Economist

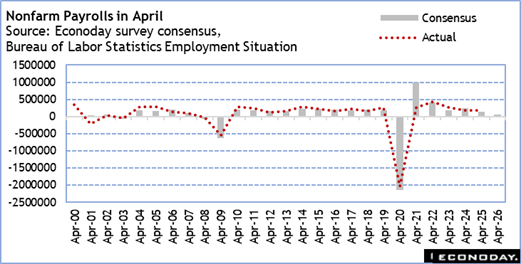

The highlight in the May 4 week will be the April employment

report at 8:30 ET on Friday. The April numbers on payrolls and the unemployment

rate could set the tone for the labor market in the second quarter of 2026.

With the conflict in Iran stretching on with no progress in concluding the

violence, businesses face ongoing geopolitical uncertainties. Businesses will

be reluctant to expand payrolls or hire into open positions. Moreover, the

upward price pressures from energy costs may lead to some layoff activity that

could accelerate if a resolution in hostilities is not reached soon.

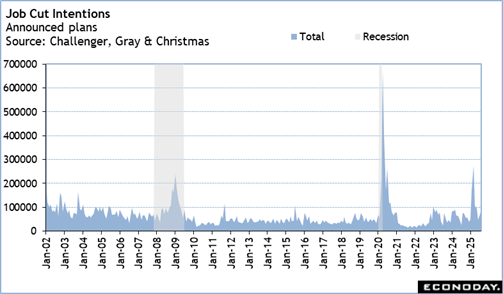

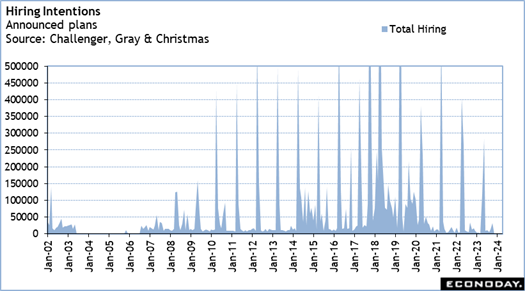

The Challenger report for job cut and hiring intentions in

April at 7:30 ET on Thursday should reflect which industries are feeling the

pinch of increased costs and worries about a return of inflationary pressures

and concerned about no relief for higher energy prices in the near term. There

may be outright layoffs and/or elimination of planned hiring. The only sector

that probably isn't affected as yet is healthcare which has been the major

source of new jobs in recent months. Hiring plans are likely top be limited to

a few sectors that normally add to payrolls in the spring largely retail and

leisure and hospitality but this could be less than usual.

While early estimates for nonfarm payrolls in April are for

tepid job gains, the April report has a strong tendency to come in below the

consensus forecast and then subsequently be revised lower in the following

month's report. April can be a tough month to forecast due to the timing of the

spring holidays, and if businesses decided to speed up hiring in March to get

ahead of the demand for seasonal workers. The survey reference week for April

is 5 weeks in 2026, so it should capture a full picture of payroll gains in the

early part of the month.

Stagnant payroll growth or even some modest declines

will affect the FOMC's outlook for monetary policy. The committee will have to

determine of a soft labor market is more of a risk to growth than rising

inflation even if the pass through from energy costs is of limited duration.

There is an interesting notice on the BLS website the

indicates that there may be an effort to backfill some of the missing data in

the consumer price index, or at least prepare for some of the consequences like

creating seasonal adjustment factors (https://www.bls.gov/bls/bls-engages-expert-panels-regarding-missing-consumer-expenditure-data.htm).

The BLS is holding public meetings with the National Association for Business

Economics (NAB) and Committee on National Statistics (CNSTAT) on May 7 and 8,

respectively.

The Week Ahead: Econoday Consensus Forecasts

Monday

US Motor Vehicle Sales for April (Any Time)

Consensus Forecast, Total Vehicle Sales - Annual Rate: 16.1

M

Consensus Range, Total Vehicle Sales - Annual Rate: 16.0

M to 16.2 M

The consensus looks for sales lower at a 16.1 million unit

rate in April from 16.3 million in March.

India PMI Manufacturing Final for April (Mon 1030

IST; Mon 0500 GMT; Mon 0100 EDT)

Consensus Forecast, Index: 55.9

Consensus Range, Index: 55.9 to 55.9

Forecasters see no revision from the flash at 55.9 for the

April final, up from 53.9 in the March final.

France PMI Manufacturing Final for April (Mon 0850

CEST; Mon 0650 GMT; Mon 0250 EDT)

Consensus Forecast, Index: 52.8

Consensus Range, Index: 52.8 to 52.8

The consensus looks for no revision from the flash at 52.8

for the April final, up from 50.0 in March

Germany PMI Manufacturing Final for April (Mon 0955

CEST; Mon 0755 GMT; Mon 0355 EDT)

Consensus Forecast, Index: 51.2

Consensus Range, Index: 51.2 to 51.2

The consensus looks for no revision from the flash at 51.2

for the April final, down from 52.2 in March.

Eurozone PMI Manufacturing Final for April (Mon 1000

CEST; Mon 0800 GMT; Mon 0400 EDT)

Consensus Forecast, Index: 52.2

Consensus Range, Index: 51.2 to 52.2

The consensus looks for no revision from the flash at 52.2

for the April final, up from 51.6 in March.

US Factory Orders for March (Mon 1000 EDT; Mon 1400

GMT)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: -0.1% to 1.0%

With durable goods orders already reported up 0.8 percent

for March, the consensus sees factory orders up a similar 0.5 percent.

Tuesday

Australia Household Spending for March (Tue 1130

AEST; Tue 0130 GMT; Mon 2130 EDT)

Consensus Forecast, M/M: 2.0%

Consensus Range, M/M: -0.5% to 2.4%

The consensus sees spending up 2.0 percent in March in

nominal terms after rising 0.3 percent in February. This gets a big boost from

the effect of higher fuel prices starting in March.

Australia RBA Announcement (Tue 1430 AEST; Tue 0430

GMT; Tue 1230 EDT)

Consensus Forecast, Change: 25 bp

Consensus Range, Change: 0 bp to 25 bp

Consensus Forecast, Level: 4.35%

Consensus Range, Level: 4.10% to 4.35%

After two straight 25 basis point increases, the RBA is

expected to raise rates by another 25 bp at this meeting as inflation remains

too hot.

Canada Merchandise Trade for March (Tue 0830 EDT; Tue

1230 GMT)

Consensus Forecast, Balance: -C$3.4 B

Consensus Range, Balance: -C$3.8 B to -C$2.0 B

The consensus sees a deficit of C$3.4billion in March after

a C$5.743 billion deficit in February.

US International Trade in Goods and Services for March (Tue

0830 EDT; Tue 1230 GMT)

Consensus Forecast, Balance: -$60.4 B

Consensus Range, Balance: -$65.2 B to -$57.6 B

Forecasters see the deficit widening to $60.4 billion in

March from $57.3 billion in February.

US PMI Composite Final for March (Tue 0945 EDT; Tue 1345

GMT)

Consensus Forecast, Composite Index: 52.0

Consensus Range, Composite Index: 52.0 to 52.0

Consensus Forecast, Services Index: 52.1

The consensus looks for no revision from the flash at 52.0

for the April composite final, up from 50.3 in March. For services, an upward revision

is expected to 52.1 from 51.3 in the flash versus 49.8 in March.

US New Home Sales for February (Tue 1000 EDT; Tue 1400

GMT)

Consensus Forecast, Annual Rate: 610 K

Consensus Range, Annual Rate: 599 K to 675K

US New Home Sales for March (Tue 1000 EDT; Tue 1400

GMT)

Consensus Forecast, Annual Rate: 668K

Consensus Range, Annual Rate: 618K to 700K

Home sales seen recovering to a 668,000 rate in March, and

to 610,000 in February from a surprisingly low 587,000 in January.

US ISM Services Index for April (Tue 1000 EDT; Tue 1400

GMT)

Consensus Forecast, Index: 53.9

Consensus Range, Index: 53.2 to 55.0

Similar to the ISM manufacturing report that was unchanged

from March to April at 52.7, the services index is seen flat at 53.9 in April

versus 54.0 in March.

Wednesday

New Zealand Labour Market Conditions for First Quarter (Wed

1045 NZST; Tue 2245 GMT; Tue 1845 EDT)

Consensus Forecast, Unemployment Rate: 5.4%

Consensus Range, Unemployment Rate: 5.3% to 5.4%

The jpbless rate is expected flat at 5.4% in Q1 versus 5.4

percent in Q4.

South Korea CPI for April (Thu 0800 KST; Wed 2300

GMT; Wed 1900 EDT)

Consensus Forecast, Y/Y: 2.5%

Consensus Range, Y/Y: 2.4% to 2.7%

CPI expected up 2.5 percent on year in April versus 2.2

percent in March.

China PMI Composite for April (Wed 0945 CST; Wed 0145

GMT; Tue 2145 EDT)

Consensus Forecast, Services Index: 52.0

Consensus Range, Services Index: 52.0 to 52.5

Services expected nearly unchanged at 52.0 in April versus

52.1 in March.

France Industrial Production for March (Wed 0845 CEST;

Wed 0645 GMT; Wed 0245 EDT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.2% to 0.5%

Output seen up 0.2 percent in March on the month versus

minus 0.7 percent in February.

France PMI Composite Final for April (Wed 0850 CEST;

Wed 0650 GMT; Wed 0250 EDT)

Consensus Forecast, Services Index: 46.5

Consensus Range, Services Index: 46.5 to 46.8

The consensus looks for no revision from 46.5 in the flash

for services.

Eurozone PMI Composite Final for April (Wed 0900 CEST;

Wed 0700 GMT; Wed 0300 EDT)

Consensus Forecast, Composite Index: 48.6

Consensus Range, Composite Index: 48.6 to 48.6

Consensus Forecast, Services Index: 47.4

Consensus Range, Services Index: 47.4 to 47.4

The consensus looks for no revision from the flash at 48.6

for the April composite final versus 50.7 in March. For services, no revision

expected from 47.4 in the flash versus 50.2 in March.

Germany PMI Composite Final for April (Wed 0955 CEST;

Wed 0755 GMT; Wed 0355 EDT)

Consensus Forecast, Composite Index: 48.3

Consensus Range, Composite Index: 48.3 to 48.3

Consensus Forecast, Services Index: 46.9

Consensus Range, Services Index: 46.9 to 46.9

The consensus looks for no revision from the flash at 48.3

for the April composite final versus 51.9 in March. For services, no revision

expected from 46.9 in the flash versus 50.9 in March.

UK PMI Composite Final for April (Wed 0930 BST; Wed 1030

GMT; Wed 0430 EDT)

Consensus Forecast, Composite Index: 52.0

Consensus Range, Composite Index: 52.0 to 52.0

Consensus Forecast, Services Index: 52.0

Consensus Range, Services Index: 52.0 to 52.0

The consensus looks for no revision from the flash at 52.0

for the April composite final versus 50.3 in March. For services, no revision

expected from 52.0 in the flash versus 50.5 in March.

US ADP Employment Report for April (Wed 0815 EDT; Wed

1215 GMT)

Consensus Forecast, Private Payrolls - M/M: 85K

Consensus Range, Private Payrolls - M/M: 40K to 140K

Payrolls seen up a decent 85K after rising 62K in March.

Thursday

Australia International Trade in Goods for March (Thu

1130 AEST; Thu 0130 GMT; Wed 2130 EDT)

Consensus Forecast, Balance: A$4.25 B

Consensus Range, Balance: A$2.0 B to A$7.5 B

The surplus expected down to A$4.25 billion in March from

A$5.586 billion in February.

Germany Manufacturing Orders for March (Thu 0800 CEST;

Thu 0600 GMT; Thu 0200 EDT)

Consensus Forecast, M/M: 1.0%

Consensus Range, M/M: -1.5% to 1.7%

Manufacturing orders are expected up another 1.0 percent on

the month in March after rising 0.9 percent in February.

Eurozone Retail Sales for March (Thu 1100 CEST; Thu 0900

GMT; Thu 0500 EDT)

Consensus Forecast, M/M: -0.1%

Consensus Range, M/M: -1.0% to 0.4%

Consensus Forecast, Y/Y: 1.3%

Consensus Range, Y/Y: 0.2% to 1.4%

Sales expected down 0.1 percent in March on the month and up

1.3 percent on year.

US Jobless Claims for Week 05/02 (Thu 0830 EDT; Thu

1230 GMT)

Consensus Forecast, Initial Claims - Level: 205K

Consensus Range, Initial Claims - Level: 190K to 215K

Claims expected to rebound to 205K in the latest week after

a surprise 26K drop to 189k a week ago.

US Productivity and Costs for First Quarter (Thu 0830

EDT; Thu 1230 GMT)

Consensus Forecast, Nonfarm Productivity - Annual Rate:

1.7%

Consensus Range, Nonfarm Productivity - Annual Rate: 1.4%

to 2.0%

Consensus Forecast, Unit Labor Costs - Annual Rate: 2.0%

Consensus Range, Unit Labor Costs - Annual Rate: 1.6%

to 3.6%

The consensus looks for productivity up 1.7 percent in Q1

and unit labor costs up 2.0 percent. In Q4 the numbers were 1.8 percent and 4.4

percent, respectively.

US Construction Spending for February (Thu 1000 EDT;

Thu 1400 GMT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.1% to 0.3%

US Construction Spending for March (Thu 1000 EDT; Thu

1400 GMT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: -0.1% to 0.6%

Construction expected to rebound by 0.2 percent in February

and another 0.4 percent on the month in March after dipping by 0.3 percent in

January.

US Consumer Credit for March (Thu 1500 EDT; Thu 1900

GMT)

Consensus Forecast, M/M: $12.0 B

Consensus Range, M/M: $10 B to $12.9 B

Expected up by a moderate $12 billion in March after

increasing by $9.5 billion in February.

Friday

Germany Industrial Production for March (Fri 0800 CEST;

Fri 0600 GMT; Fri 0200 EDT)

Consensus Forecast, M/M: -0.2%

Consensus Range, M/M: -1.5% to 3.0%

Consensus Forecast, Y/Y: -2.5%

Consensus Range, Y/Y: -3.7% to -1.7%

Sales seen down 0.2 percent on month in March and down a

dismal 2.5 percent on year.

Germany Merchandise Trade for March (Fri 0800 CET;

Fri 0600 GMT; Fri 0200 EDT)

Consensus Forecast, Balance: E16.5 B

Consensus Range, Balance: E14.0 B to E20.1 B

The consensus sees the surplus down at E16.5 billion versus

E19.8 billion in February.

Canada Labour Force Survey for April (Fri 0830 EDT;

Fri 1230 GMT)

Consensus Forecast, Employment - M/M: 16K

Consensus Range, Employment - M/M: 6K to 25K

Consensus Forecast, Unemployment Rate: 6.7%

Consensus Range, Unemployment Rate: 6.6% to 6.7%

Employment bouncing back a bit in March and April from

losses early in January and February but not enough to move the jobless rate

from 6.7 percent in April.

US Employment Situation for April (Fri 0830 EDT; Fri

1230 GMT)

Consensus Forecast, Nonfarm Payrolls - M/M: 63K

Consensus Range, Nonfarm Payrolls - M/M: 0 to 150K

Consensus Forecast, Unemployment Rate: 4.3%

Consensus Range, Unemployment Rate: 4.2% to 4.4%

Consensus Forecast, Private Payrolls - M/M: 67K

Consensus Range, Private Payrolls - M/M: 40K to 95K

Consensus Forecast, Average Hourly Earnings - M/M: 0.3%

Consensus Range, Average Hourly Earnings - M/M: 0.2%

to 0.3%

Consensus Forecast, Average Hourly Earnings - Y/Y: 3.8%

Consensus Range, Average Hourly Earnings - Y/Y: 3.6%

to 3.8%

Consensus Forecast, Average Workweek: 34.2

Consensus Range, Average Workweek: 34.2 to 34.3

A moderate increase of 63K is the call for nonfarm payrolls

with the jobless rate flat at 4.3 percent.

US Consumer Sentiment for May (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, Index: 49.3

Consensus Range, Index: 48.0 to 53.0

Sentiment expected to slip to 48.6 in the first report for

May from an already gloomy 49.8 in the April final as consumers are unhappy

about rising prices for gas and worried about the economic outlook.

|